Propel provides innovative insurance solutions to thousands of companies across the country. We make it our business to know your world inside and out.

Commercial, Insights, Real Estate

Evolving Skylines: A Shifting Property Insurance Market – What Real Estate Owners Should Do While Conditions Soften

After several years of tightening conditions, the property insurance market is showing meaningful signs of relief. For real estate owners, operators, and boards—particularly those managing multifamily, industrial, and commercial property portfolios—this shift presents a rare opportunity to reassess coverage, pricing, and long-term risk strategy.

The Property Market Is Softening—But Not Uniformly

The property insurance market is cyclical, and current conditions suggest we are transitioning out of a prolonged hard market.

According to Alera Group’s 2026 Property & Casualty Market Outlook Report, the market is entering a period of recalibration. While challenges remain, especially for certain property classes and geographies, the balance of power is beginning to move back toward buyers.

Several forces are contributing to this shift:

- Fewer catastrophic loss events in 2025 resulted in lower industry loss activity than in prior years.

- Improved insurer profitability, supported by rate adequacy and stronger underwriting results, has increased carriers’ willingness to compete.

- Fresh capital entering the insurance and reinsurance markets has expanded overall capacity.

For well-managed, well-documented real estate risks, this environment is driving increased competition among insurers and greater underwriting flexibility.

That said, the current market softening is not universal. Properties with poor loss histories, aging infrastructure, coastal or catastrophe-exposed locations, or governance challenges may still face underwriting and rate challenges.

Increased Capacity Is Compressing Rates and Expanding Terms

One of the most significant developments for property owners is the influx of capacity into the market. As new insurers and capital providers compete for market share, pricing pressure is easing, particularly in commercial property coverage.

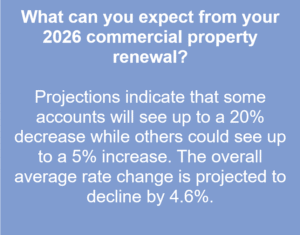

The 2026 Market Outlook projections suggest commercial property rates ranging from substantial decreases to modest increases, with many accounts seeing flat to favorable outcomes.

Competition is also driving:

- Broader coverage terms

- Higher available limits

- Renewed availability of coverages that were previously restricted or unaffordable

If your real estate organization invested in risk management during the hard market, now is your chance to realize a return on your investment in the form of more favorable coverage.

Reinsurance Renewals Are Improving Buyer Leverage

Reinsurance plays a critical role in shaping property insurance pricing and availability. Recent treaty renewals have come in at negative percentages, making it less expensive for insurers to transfer risk.

As reinsurance pricing stabilizes and capacity remains plentiful, primary carriers gain flexibility, often passing those benefits downstream to insureds through improved pricing and structure. Underwriters remain disciplined and will want to see evidence of risk management. However, the pace of rate increases has slowed, particularly outside the most catastrophe-exposed regions.

London Markets Continue to Influence Domestic Property Insurance

The London insurance market remains a major force in property underwriting, especially for layered programs, excess placements, and catastrophe-exposed risks. As London markets apply pressure on domestic carriers through pricing benchmarks, capacity decisions, and risk appetite, U.S. insurers are adjusting their strategies accordingly.

For real estate buyers who need coverage layers or have hard-to-insure risks, the interplay between the London market and U.S. carriers can complicate insurance. However, with strategic program design and strong broker advocacy, it’s possible to navigate domestic and international market dynamics successfully.

Strategic Takeaways for Real Estate Organizations

Softening conditions do not eliminate risk, but they do create opportunity. Real estate owners and boards should consider the following actions:

- Re-evaluate coverage structure. This may be an ideal time to restructure layers, revisit deductibles, or explore alternatives that were previously cost-prohibitive.

- Differentiate risk quality. Underwriters are competing for best-in-class accounts. Clear documentation, proactive maintenance, and strong governance matter more than ever.

- Start renewal discussions early. Improved conditions favor those who plan ahead and present a thoughtful, complete submission.

- Avoid complacency. Even in a softer market, coverage terms, exclusions, and sublimits continue to evolve. Assumptions can lead to gaps.

As property market conditions begin to soften, the real opportunity for real estate owners is not just lower premiums but better program design, stronger coverage, and smarter long-term risk positioning. While softening conditions will not last forever and not every risk will benefit equally, organizations that act early, understand their leverage, and partner with experienced advisors are best positioned to gain the most.

Propel’s Real Estate Group helps clients navigate both opportunity and complexity, turning market shifts into smarter, more resilient insurance strategies.

Sources: 2026 Alera Group P&C Market Outlook. Published December 2025

Melody Olson

Melody has spent over 20 years specializing in real estate, construction, and project risk insurance. Melody is known by clients and colleagues for having strong technical expertise, creative problem-solving skills, and relentless client advocacy. More about Melody...

Brynnan Hyland

With over a decade of industry experience, Brynnan brings a strong underwriting background with a focus on complex risks and program design. By analyzing client risk profiles and tailoring coverage solutions, Brynnan delivers clear guidance and a strategic approach to risk management.